Where this engagement started

The business is a US manufacturer-distributor with a Malaysian parent group. The parent group's

industrial credibility was real. The US-side public surface, the brand, the website, the catalogue, and

the channel, did not match it. Market expansion was stalling on the basics: buyers landed on a stale

catalogue they could not navigate, enquiries scattered across inboxes, no clean path from a web enquiry to

the warehouse, and no way for retail or small-volume buyers to buy from the business directly without

going through an aftermarket reseller.

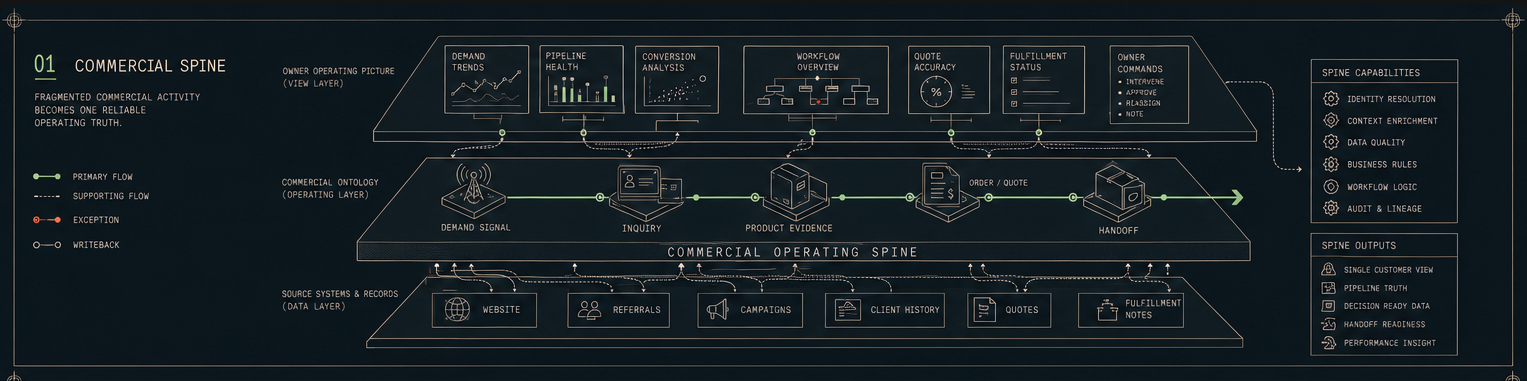

The brief opened as a commercial operating spine: catalogue, brand, website, lead routing. It expanded as

the work progressed: a public pricing transparency layer for buyers, a direct-to-consumer storefront

alongside the existing distribution channel, and pricing intelligence that surfaced the geographic

pricing variance the owner had not yet seen. One operator stayed deep in the work, end to end.

Nine pieces of work, one operator

1. Brand and creative. The original public surface did not match the parent group's

industrial reputation. The identity system was rebuilt so the brand entered conversations on the same

footing as the parent group's operations.

2. Public website. The new site went live on a modern, accessible stack: fast on

mobile, accessible to all visitors, and indexed cleanly. The site is the credibility baseline.

Everything else builds on top of it.

3. Catalogue system. The full SKU catalogue was migrated, the taxonomy enriched, every

measurement verified. Buyers landing on the catalogue can search, filter, and find the right part. Without

a clean catalogue, there is no clean spine.

4. Lead-to-fulfilment spine. Every web form enquiry and every inbound email is

captured before any human-sales-desk filter, parsed to extract the part, the company, the quantity, and

the urgency, and pushed through to the warehouse system as a sales order the warehouse can pick, pack,

and ship. The handoff is observable to the team and traceable end-to-end. Email enquiries get a drafted

acknowledgement so qualified prospects do not go dark while a human is still at lunch.

5. Demand-sensing engine. Search analytics, market data, and the industry registry are

consolidated into one layer. The owner can see what buyers are searching for, what the market is paying,

where the business is invisible to demand it should be capturing, and which products and geographies are

the highest-value gaps to close first.

6. Pricing intelligence. An internal report compares the business's current pricing

against external market benchmarks for the top SKUs. The same layer shows geographic-pricing variance

and freight-cost arbitrage: where regional pricing differences combined with absorbed freight cost are

quietly bleeding margin, and whether nationwide or regional pricing is the right model going forward.

7. Factory-direct value calculator. A public-facing pricing transparency layer lets

buyers see what they save by buying direct from the manufacturer instead of going through an aftermarket

reseller. Industry-aggregate markup citation, no competitor naming. The buyer leaves the page with a

concrete number, not a marketing claim.

8. Direct-to-consumer storefront. A retail commerce path lets small-volume buyers buy

from the business directly, alongside the existing distribution channel. It routes to the same warehouse

system as the B2B spine, with retail and B2B orders tagged at the point of fulfilment so finance can

attribute revenue cleanly.

9. Channel and expansion. A regional market expansion is in flight. Marketplace

positioning and a commerce channel are being built out alongside it. The same engagement shape is being

scoped for the parent group's adjacent-region operations.

This is operate-with mode. The operator stays deep in the business and moves wherever the work needs to

move. It is not one deliverable. It is one trusted person keeping brand, systems, data, channels,

pricing, retail, and owner review connected.

How the engagement is sequenced

The engagement opened with brand and website to set the credibility baseline. Without those, the rest of

the work has no foundation. Catalogue migration came next as the basis for the lead-to-fulfilment spine.

Lead routing was wired through to the warehouse before any public launch: the website does not go live

until the warehouse can fulfil what the website captures.

Demand-sensing layered on top once the routing was reliable. Pricing intelligence and the factory-direct

calculator followed as the proof base grew. The direct-to-consumer storefront comes last in the

public-facing layer because retail traffic depends on a clean catalogue, working fulfilment, and pricing

transparency already being in place.

Sequencing is the architecture: each layer carries the trust the next layer inherits. A clean catalogue

does not help if the brand still looks stale, and a retail storefront does not help if the warehouse

cannot ship what it sells. The work was sequenced so each stage built the foundation for the next.

Why the safety rules exist

When automations touch outside systems, the warehouse, the catalogue, the buyer's inbox, the payment

processor, the failure modes are different from internal automation. A misfire reaches a buyer; a

misclassified enquiry routes to the wrong team; a too-aggressive scrape gets blocked; a retail order in

the wrong fulfilment queue makes the business look unserious.

The engagement codifies safety rules into how this work runs. Explicit guardrails on which third-party

systems an automation can touch, explicit review steps before any outbound action, explicit logging of

every external call, and per-row human review on the lead-to-fulfilment spine until trust accrues. The

client is never load-bearing for whether the automation behaved itself. That is the difference between a

forward-deployed operator and a dev shop running scripts.